The average annual cost of homeowners insurance in the United States is approximately $2,110 for $300,000 of dwelling coverage, but rates vary by state.

Homeowners insurance costs an average of $2,110 per year, or roughly $176 per month, according to a US-based research and analysis firm.

We analysed pricing data from over 100 insurance firms to determine the average cost of homeowners insurance in each state and the main U.S. cities. Our sample insurance was for a 40-year-old homeowner with good credit, $300,000 in dwelling and liability coverage, and a $1,000 deductible.

Please keep in mind that the rates mentioned in this article are only benchmarks. The cost of homeowners insurance will vary depending on your region, property size, and the amount of coverage you require.

How much is home insurance in your state?

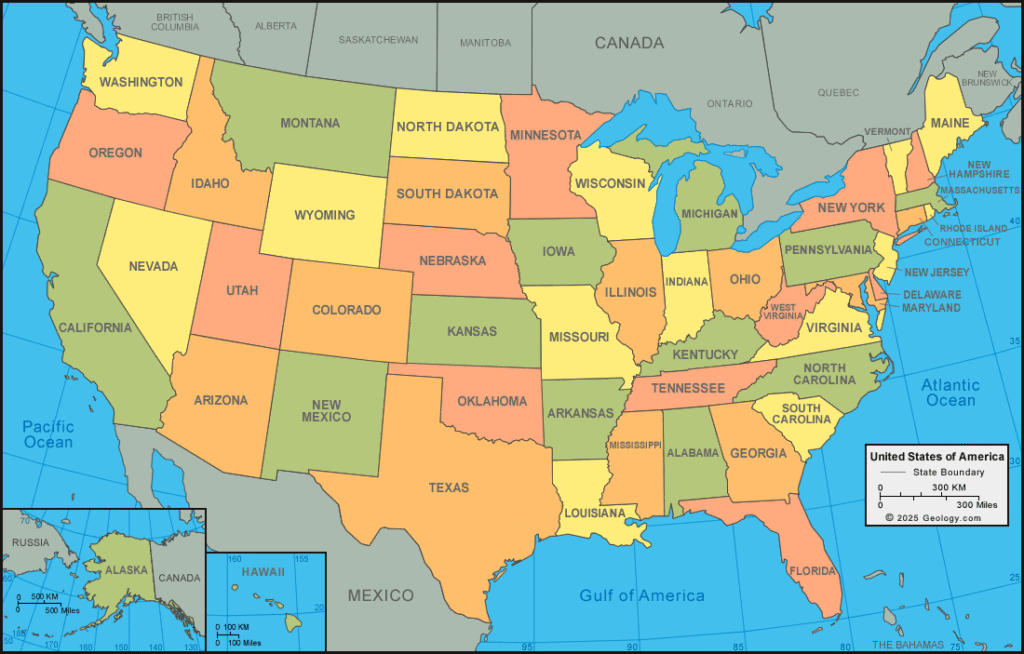

Average homes insurance rates vary greatly, and where you reside has a significant impact on how much you pay for homeowners insurance. Hover over your state on the map below to see the average home insurance price.

Average home insurance prices by state.

These are the most expensive states for homeowners insurance.

Oklahoma: $6,210 a year, or about $518 a month, on average.

Texas: $4,585 a year, or about $382 a month, on average.

Nebraska: $4,505 a year, or about $375 a month, on average.

Colorado: $4,175 a year, or about $348 a month, on average.

Kansas: $3,735 a year, or about $311 a month, on average.

Here are the cheapest states for homeowners insurance.

Hawaii: $610 a year, or about $51 a month, on average.

Vermont: $950 a year, or about $79 a month, on average.

Delaware: $1,025 a year, or about $85 a month, on average.

Alaska: $1,035 a year, or about $86 a month, on average.

Maine: $1,180 a year, or about $98 a month, on average.

Here are the typical annual and monthly house insurance costs in all 50 states plus Washington, D.C.

| State | Average annual cost | Average monthly cost |

| National average | $2,110 | $176 |

| Alabama | $3,420 | $285 |

| Alaska | $1,035 | $86 |

| Arizona | $2,565 | $214 |

| Arkansas | $3,215 | $268 |

| California | $1,335 | $111 |

| Colorado | $4,175 | $348 |

| Connecticut | $1,870 | $156 |

| Delaware | $1,025 | $85 |

| Florida | $2,625 | $219 |

| Georgia | $2,435 | $203 |

| Hawaii | $610 | $51 |

| Idaho | $1,460 | $122 |

| Illinois | $2,420 | $202 |

| Indiana | $2,495 | $208 |

| Iowa | $2,505 | $209 |

| Kansas | $3,735 | $311 |

| Kentucky | $2,510 | $209 |

| Louisiana | $2,220 | $185 |

| Maine | $1,180 | $98 |

| Maryland | $1,945 | $162 |

| Massachusetts | $1,595 | $133 |

| Michigan | $2,095 | $175 |

| Minnesota | $2,920 | $243 |

| Mississippi | $3,310 | $276 |

| Missouri | $3,290 | $274 |

| Montana | $2,735 | $228 |

| Nebraska | $4,505 | $375 |

| Nevada | $1,305 | $109 |

| New Hampshire | $1,185 | $99 |

| New Jersey | $1,290 | $108 |

| New Mexico | $1,730 | $144 |

| New York | $1,740 | $145 |

| North Carolina | $2,490 | $208 |

| North Dakota | $2,805 | $234 |

| Ohio | $1,590 | $133 |

| Oklahoma | $6,210 | $518 |

| Oregon | $1,305 | $109 |

| Pennsylvania | $1,440 | $120 |

| Rhode Island | $2,080 | $173 |

| South Carolina | $2,350 | $196 |

| South Dakota | $3,345 | $279 |

| Tennessee | $2,850 | $238 |

| Texas | $4,585 | $382 |

| Utah | $1,385 | $115 |

| Vermont | $950 | $79 |

| Virginia | $1,705 | $142 |

| Washington | $1,415 | $118 |

| Washington, D.C. | $1,295 | $108 |

| West Virginia | $1,770 | $148 |

| Wisconsin | $1,515 | $126 |

| Wyoming | $1,555 | $130 |

How much is homeowners insurance in your city?

We analysed rates in 20 of the largest metropolitan areas in the United States to determine the average cost of homeowners insurance in each location. Houston had the highest average rate, at $6,370 per year. San Jose, California, was the most affordable city on the list, with an average annual fee of $1,090.

| City | Average annual cost | Average monthly cost |

| Atlanta | $2,620 | $218 |

| Austin | $3,400 | $283 |

| Chicago | $2,750 | $229 |

| Dallas | $4,945 | $412 |

| Denver | $4,735 | $395 |

| Fort Worth, Texas | $5,825 | $485 |

| Houston | $6,370 | $531 |

| Indianapolis | $2,760 | $230 |

| Las Vegas | $1,390 | $116 |

| Los Angeles | $1,570 | $131 |

| Miami | $5,095 | $425 |

| Minneapolis | $2,995 | $250 |

| New York | $2,295 | $191 |

| Orlando | $2,510 | $209 |

| Philadelphia | $2,155 | $180 |

| Phoenix | $3,150 | $263 |

| San Antonio | $3,845 | $320 |

| San Diego | $1,305 | $109 |

| San Jose, California | $1,090 | $91 |

| Seattle | $1,365 | $114 |

Average homeowners insurance cost by company

We determined the average annual premiums for some of the largest homeowners insurance companies in the United States based on market share. It’s worth noting that some may not offer homeowners insurance in your state. To read our reviews of each company, click on their names.

| Company | Average annual cost | Average monthly cost |

| Travelers | $2,055 | $171 |

| State Farm | $2,185 | $182 |

| Allstate | $2,380 | $198 |

| Farmers | $2,600 | $217 |

| Nationwide | $2,610 | $218 |

| American Family | $2,745 | $229 |

| USAA* | $1,790 | $149 |

| *USAA homeowners insurance is available only to active-duty military, veterans and their families. | ||

Average home insurance cost by dwelling coverage amount

The amount of dwelling coverage you require is a major element in determining how much your homeowners insurance will cost. Dwelling coverage is the portion of your insurance that pays to reconstruct the structure of your house in the event that it is damaged or destroyed.

If your home is large or has high-end features, it will cost more to rebuild and require more dwelling coverage. The following are the average house insurance costs for four levels of coverage.

| Dwelling coverage amount | Average annual insurance cost |

| $200,000 | $1,555 |

| $300,000 | $2,110 |

| $400,000 | $2,655 |

| $500,000 | $3,210 |

Average homeowners insurance cost by home age

Older homes are sometimes more expensive to insure than modern homes because they lack the safety measures that newer homes have, and maintenance can be pricey. Compare the average annual cost of insuring a new home to an older home. (The coverage restrictions were the same in all three houses.

| Year home was built | Average annual insurance cost |

| 1955 | $2,110 |

| 1984 | $2,110 |

| 2024 | $1,220 |

Average homeowners insurance cost by deductible

A house insurance deductible is the amount you must pay for a claim before it is covered by your insurer. Typically, a higher deductible results in lower home insurance rates.

| $1,000 deductible | $2,500 deductible | Difference |

| $2,110 | $1,865 | -12% |

Average homeowners insurance cost based on claims history.

If you have previously filed homeowners insurance claims, insurers may view you as a higher risk and raise your premiums as a result. Here’s how making a claim may effect your homeowners insurance costs.

| No claims | 1 claim | Difference |

| $2,110 | $2,305 | 9% |

Average homeowners insurance cost by credit

According to studies, people with weak credit are more likely to file claims, so in most states, homeowners with poor credit will pay extra for home insurance. Read more about how credit scores affect house insurance prices.

(Note that California, Maryland, and Massachusetts do not allow the use of credit to set homeowners insurance costs.)

| Good credit | Poor credit | Difference |

| $2,110 | $3,620 | 72% |

Other factors that impact the cost of home insurance

Your house insurance prices will also be affected by the following factors:

Your location – Living closer to a fire station can reduce your premiums, however living in a high-crime neighbourhood may raise them.

Your risk of natural disasters – If you reside in a location prone to wildfires, tornadoes, or hurricanes, your house insurance premiums may be higher.

Extra features – Swimming pools and trampolines may be enjoyable for the whole family, but some insurers view them as possible liability claims and may charge you more to insure your house as a result.

Your dog – Some insurers may demand an additional fee for animal liability coverage, while others will not cover breeds they believe to be at risk or dogs with a history of aggressiveness. Learn more about dog and home insurance.

Why is home insurance getting more expensive?

If your house insurance premiums have increased in recent years, you are not alone. According to a 2025 USA business Nerd Wallet survey of over 1,300 U.S. homeowners performed online by The Harris Poll, 54% of them report that their insurance prices have increased in the last year. Premiums have been increasing for several years, owing to a combination of inflation and natural calamities.

Inflation does not only effect petrol and food prices. Homeowners insurance rates are rising as the cost of repairing and rebuilding damaged homes has increased. That is why, even if you have not made any recent claims, your homeowners premium may increase at your next renewal.

Homeowners insurance rates are rising especially swiftly in areas of the country where natural disasters such as tornadoes, hurricanes, and wildfires are becoming more frequent. According to the National Oceanic and Atmospheric Administration, more than 25 separate catastrophes in 2024 cost at least $1 billion in losses each.

How to reduce the cost of homeowners insurance

Shop around.

Getting house insurance quotes on an annual basis is the best method to ensure you are still getting the best bargain. We recommend that you compare quotes from at least three companies. To achieve a fair comparison, make sure the coverage limits and deductibles are identical across all three insurance.

If you don’t want to shop around yourself, ask an independent agent or broker to collect quotations on your behalf.

Raise your deductible

A greater deductible indicates a lower rate. According to NerdWallet’s rate analysis, increasing your deductible from $1,000 to $2,500 can save you almost 12% each year on average. If you need to file a claim, be sure you have enough cash on hand to cover the costs.

Ask about discounts.

Many insurers offer discounts to help customers get lower homeowners insurance rates, such as:

Multiple policies – If you combine your homeowners insurance with another policy, such as auto insurance, you may be eligible for a discount. Discover the greatest home and auto combos.

Safety and security devices – Installing fire alarms, deadbolts, security cameras, and other protective equipment in your home could help you save money. Some companies also provide discounts on specific smart-home products.

Claims-free – Many insurers give discounts to homeowners who haven’t filed a claim in three to five years.

Upgrade your home.

Certain upgrades, such as replacing an electrical or plumbing system, may result in decreased homeowner insurance prices. Getting a new roof may also result in a reduction, especially if it is resistant to wind and hail.

Build your credit.

Most states allow insurers to establish premiums based on your credit-based insurance score (which is similar to your FICO score). Some studies have found a link between low credit and filing claims, so those with a checkered credit history may pay extra for homes insurance. Building your credit may take some time, but it might save you a lot of money on homes insurance in the long term.

California, Maryland, and Massachusetts do not allow the use of credit to set homeowner, renters, condo, or mobile home insurance costs.

FAQs

Why is home insurance so expensive?

Your homeowners insurance may cost more than you expect if your home is older, your area is prone to natural catastrophes, or you have low credit, among other considerations. Climate change is also increasing the severity of certain sorts of disasters, prompting insurers to raise their rates. However, each insurance company’s policy premiums vary slightly. If you’re dissatisfied with your current rate, obtain quotations from at least three other businesses to see if you can get a better bargain.

How can I save money on homeowners insurance?

Most carriers provide savings if you purchase multiple policies or protect your house with a burglar alarm or sprinkler system. Choosing a higher deductible can also save you money, as long as it is an amount that can be covered in the event of a calamity.

Is home insurance cheaper if you pay yearly?

Some businesses provide reductions if you pay your premium in full up front rather than in monthly payments.

Check out Why U.S. investors are exploring Mumbai:

Explore Indian properties today – View Luxury Homes in Mumbai »